Looking at a mortgage offer can feel like reading a puzzle. You see a final monthly payment, but it’s a bundle of different costs, and it’s not always clear what you’re really paying for. Most homeowners just know the final number, not what’s inside it.

But if you’re self-employed, the bigger challenge often isn’t understanding the payment—it’s getting approved for it in the first place.

This guide will solve both problems.

First, we’ll break down the simple formula behind every mortgage payment. Second, we’ll show you exactly how to get a mortgage for self-employed borrowers, even if your tax returns don’t show your full income.

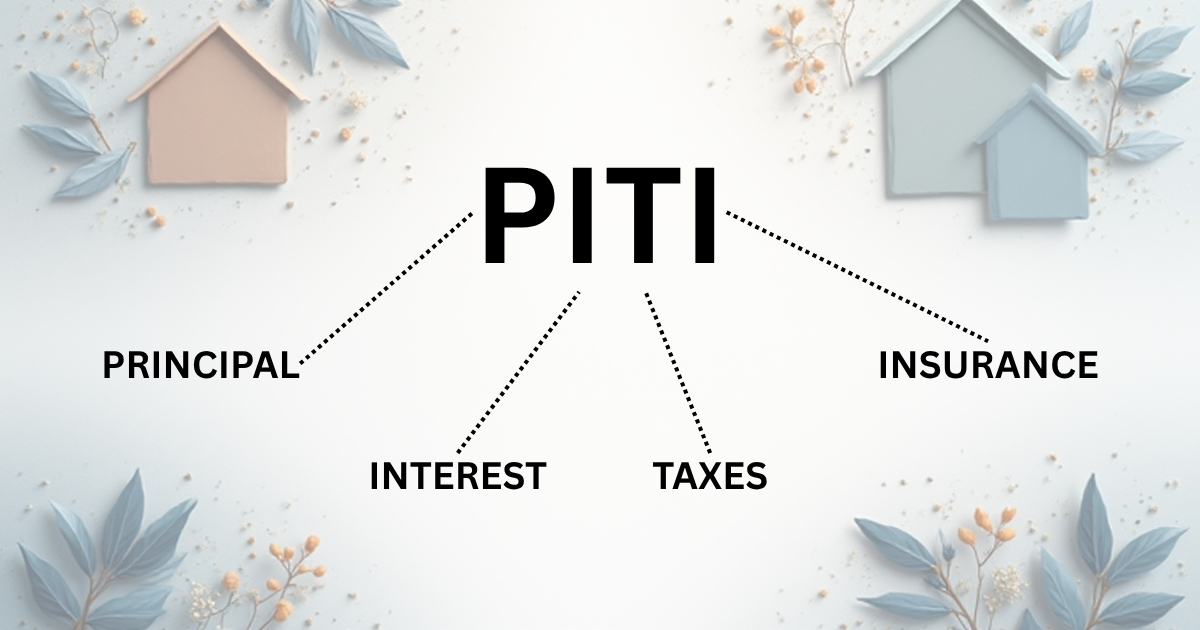

The 4-Letter Formula: How Your Mortgage Payment Is Calculated (PITI)

When lenders and real estate pros talk about a mortgage payment, they live by a four-letter acronym: PITI.

Your entire monthly payment is just these four things added together.

P = Principal

This is the actual money you borrowed. Every time you make a principal payment, you are paying down your loan balance and building equity (which is the part of the home you truly own). At the beginning of your loan, most of your payment goes to interest. In the end, it’s almost all principal.

I = Interest

This is the fee you pay the bank for lending you the money. Your interest rate is one of the most powerful factors in your monthly payment. A lower rate, even by a single percentage point, can save you hundreds of dollars per month and tens of thousands over the life of your loan.

T = Taxes

These are your local property taxes. Your lender doesn’t want you to forget to pay them (if you don’t, the government could put a lien on your house), so they handle it for you.

Your lender takes your estimated annual property tax bill, divides it by 12, and adds that amount to your monthly payment. They hold this money in a separate account called an escrow account and pay your tax bill for you when it’s due.

I = Insurance

This part is actually two things:

- Homeowner’s Insurance: This is mandatory. It protects your home (and the bank’s investment) from things like fire, theft, or natural disasters. Like taxes, your lender collects 1/12th of your annual insurance premium and pays the bill for you from your escrow account.

- Private Mortgage Insurance (PMI): If you make a down payment of less than 20%, your lender will almost always require you to pay PMI. This insurance doesn’t protect you—it protects the lender in case you stop paying. It’s an extra monthly fee that typically goes away automatically once your loan-to-value ratio reaches 80% (meaning you have 20% equity).

So, the formula is simple: Principal + Interest + Taxes + Insurance = Your Total Monthly Payment.

The Lender’s Side: How They Decide What You Can Afford

Knowing what’s in your payment is half the battle. The other half is proving to a lender that you can actually pay it.

Lenders focus on one thing above all else: Risk. To measure that risk, they look at two key numbers.

Your Debt-to-Income (DTI) Ratio: The Only Number That Matters

Your DTI is a percentage that shows how much of your gross monthly income (before taxes) goes toward paying your monthly debts.

Here’s the simple math: (All Monthly Debts + Your New PITI Payment) / Your Gross Monthly Income = DTI

Your “monthly debts” include car payments, student loans, and credit card minimum payments. Lenders want to see a DTI of 43% or lower, though some programs are more flexible.

Why Your Credit Score Is Your Key to a Lower Payment

Your credit score does more than just get you a “yes” or “no.” It directly controls the “I” (Interest) in your PITI.

A higher credit score signals to lenders that you are a low-risk borrower. To compete for your business, they will offer you a lower interest rate. A lower rate means a lower monthly payment and a lot less money paid over the 30-year loan.

The Ultimate Guide to Getting a Mortgage for Self Employed

Here’s the frustrating truth for entrepreneurs: the very tax write-offs your accountant loves are what make mortgage lenders nervous.

Your goal at tax time is to show as little income as possible to pay less in taxes. But your goal at mortgage time is to show as much income as possible to qualify for a loan.

So, how do you bridge the gap?

The “Problem”: Why Lenders See Risk (and You See Success)

A W-2 employee has a predictable paycheck. A lender can easily verify their $60,000 salary.

A self-employed person’s income is variable. Worse, if you made $150,000 in revenue but wrote off $100,000 in expenses (cars, travel, supplies, etc.), your tax return says you only made $50,000. To a lender, your income is $50,000.

How Lenders Actually Calculate Your Self-Employed Income

Lenders don’t look at your bank statements (at first). They look at your federal tax returns, specifically your Schedule C (for sole proprietors) or your K-1s (for S-Corps/partnerships).

Here’s the formula they use:

- They use the 2-Year Rule: Lenders average the net income (after-expense) from your last two years of tax returns.

- (Year 1 Net Income + Year 2 Net Income) / 24 = Your “Official” Monthly Income

The Pro-Tip: “Adding Back” Depreciation. A good loan officer will know how to help you. Lenders will often “add back” certain paper-loss expenses like depreciation (for a vehicle or large equipment). Because this isn’t real money leaving your account each month, they can add it back to your net income, helping you qualify for more.

Can’t Show Enough Income? Bank Statement Loans Are Your Answer

What if your tax returns are just too low? You’re not stuck.

Ask a lender about a Bank Statement Loan.

This is a special program (often called a “non-QM” loan) designed for self-employed borrowers. Instead of tax returns, these loans use 12 or 24 months of your business bank statements to verify your cash flow. They will average your monthly deposits to determine your qualifying income.

The Trade-Off: These loans are seen as higher-risk, so you must be a strong borrower. The trade-off is a higher interest rate and often a larger down payment (10-20% is common).

5 Steps to Prepare Your Self-Employed Mortgage Application

- Keep Your Books Clean. Have separate bank accounts for your business and personal expenses. This is non-negotiable.

- Talk to a Lender Before Tax Season. This is the most common mistake I see. Your accountant’s job is to save you money today. Your mortgage broker’s job is to get you a loan tomorrow. Tell them you plan to buy a home so they can advise you on how many write-offs to take.

- Pause on Big Purchases. Don’t buy a new truck or expensive equipment for the business within six months of applying for a loan. That new monthly payment will directly harm your DTI ratio.

- Boost Your Down Payment. A larger down payment (especially 20% or more) reduces the lender’s risk and makes you a much stronger applicant.

- Find the Right Partner. Don’t just go to any big bank. Find a mortgage broker who has experience with self-employed borrowers. They will know which lenders have the best programs (like bank statement loans) for your specific situation.

Your Next Steps: From Confused to Confident Homebuyer

Getting a mortgage doesn’t have to be a mystery.

Understanding how your mortgage payment is calculated (PITI) is the first step to taking control of your finances.

And if you’re self-employed, proving your income isn’t a roadblock—it just means you need a different map. By keeping clean books and finding a lender who understands entrepreneurship, you can turn your business success into a new home.

I’m a tech-savvy writer and passionate software engineer who loves exploring the intersection of technology and creativity. Whether it’s building efficient systems or breaking down complex tech topics into simple words, I enjoy making technology accessible and useful for everyone.